Non Dividend Distribution とは

投稿日:

米国の証券会社で資金を運用されている方の申告を請け負いますが、幾つか気を付けなければならないポイントがあります。

Non-Dividend Distribution ですが、Dividend(配当)として表示されてますが、出資金額の元金部分の払い戻し(資本金の払い戻し)ですので、原則として、配当所得とはなりません。

以下 https://taxmap.irs.gov/taxmap2018/pub17/p17-037.htm から抜粋

A nondividend distribution is a distribution that isn’t paid out of the earnings and profits of a corporation or a mutual fund. You should receive a Form 1099-DIV or other statement showing the nondividend distribution. On Form 1099-DIV, a nondividend distribution will be shown in box 3. If you don’t receive such a statement, you report the distribution as an ordinary dividend.

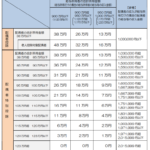

Example. (p64)

関連記事

-

-

今年の年末調整は再計算が大幅増加か?配偶者控除、配偶者特別控除の計算要注意(水曜勉強会)

2018年12月からの年末調整計算については再計算の対象者が増えそうです。201 …

-

-

海外で中古木造物件を購入して節税

例えばハワイで木造の賃貸物件を購入すると、日本での節税につながるというスキームを …

-

-

寄付金課税に新たな解釈(水曜勉強会)

今日の勉強会は、わたくし、山沢が講師を務める出番でした。 マイナン …

-

-

租税滞納状況 税金の滞納そんなに多いの?(水曜勉強会)

今日の勉強会の講師は岩里さん。空き家譲渡特例、企業版ふるさと納税、国外転出課税、 …

-

-

なぜパナマ文書があそこまで注目されたのか?BEPSプロジェクトとの関係(新聞報道を解説)

なぜパナマ文書があそこまで報道され、特にヨーロッパ中心に税務情報開示の透明化が一 …

-

-

バンコク事務所のサイトをリニューアルしました。

http://www.almetasia.com/

-

-

タックスヘイブン対策税制の対象となる国

法人税率が20%以下の国に子会社を設立すると、「タックスヘイブン対策税制」という …

-

-

消費税計算端数処理はどうする?

商品の価格は、原則として消費税を含めた総額で表示しなければなりません。これは「消 …

- PREV

- 事業継続緊急対策(テレワーク)助成金が登場

- NEXT

- 1099-INT Treasury Note